Silas North · Field Notes From Enough · June 18, 2026

Silas North · Field Notes From Enough · June 18, 2026There is a kind of financial product that looks noble for decades and then starts behaving like a houseguest who has forgotten where the door is. Permanent life insurance can be one of them.

Not always. Not for everyone. Say that clearly before the compliance people start warming up the printer.

Life insurance has a real purpose. During your working years, it can protect a spouse, children, a mortgage, a business partner, or a family balance sheet that would get knocked sideways by an untimely death.

But responsible decisions have expiration dates.

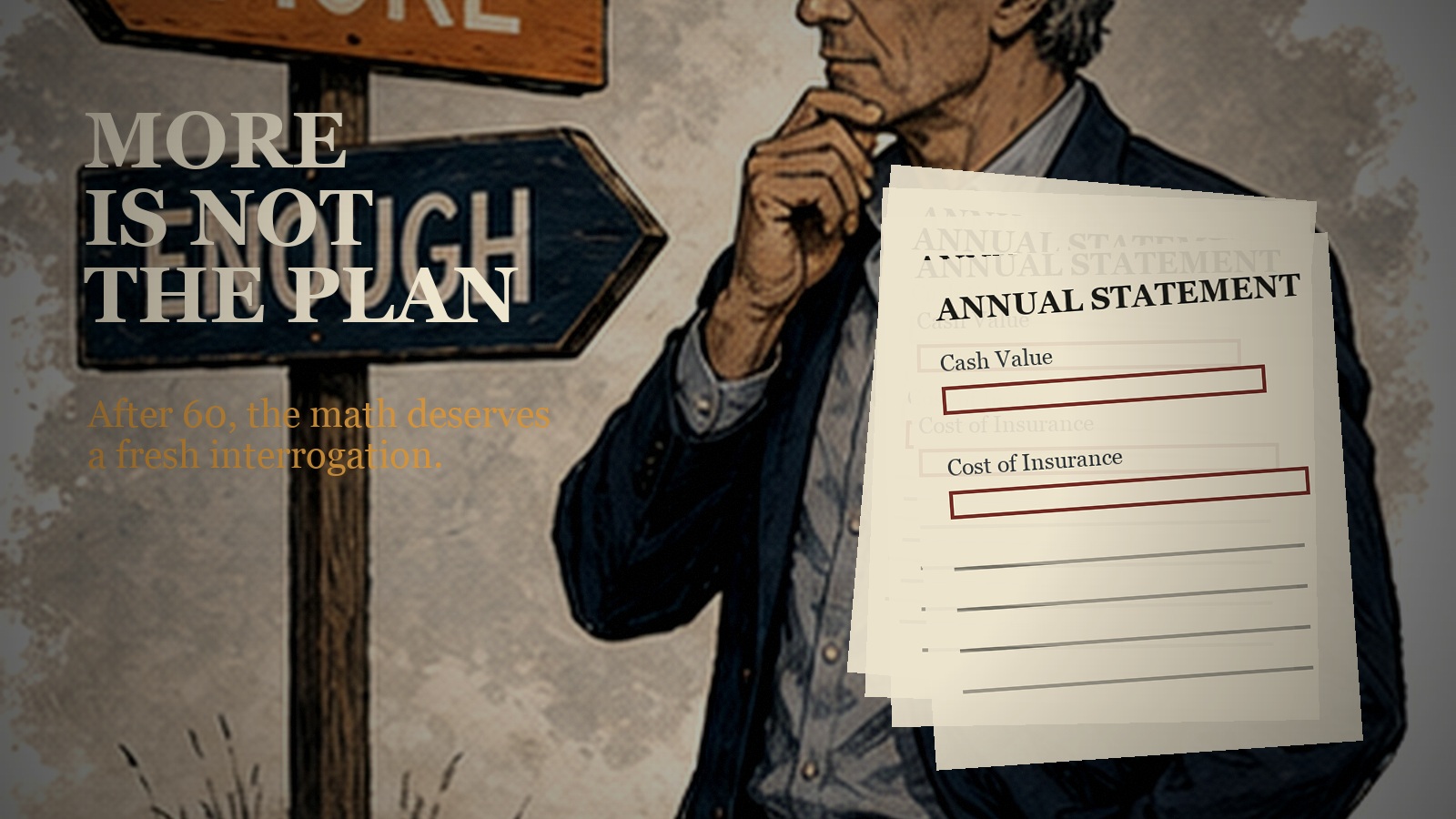

After 60, the question changes. It is no longer, “Was this policy a good idea when I bought it?”

The better question is simpler:

Does this policy still serve my life now, or am I serving it?

That is where things get interesting. And by interesting, I mean expensive. Finance has a gift for making unpleasant math wear a necktie.

The Quiet Problem Inside Older Policies

Many permanent life insurance policies build cash value over time. That sounds comforting. You paid in for years. On paper, it feels like a private reserve inside the contract.

But inside many policies, especially universal life and certain permanent contracts, another machine is running.

The cost of insurance rises as you age.

That is not a moral judgment. It is actuarial gravity. Mortality risk goes up. After 60, those charges can become meaningfully higher.

Often, that monthly cost is deducted from cash value. You may not feel it because you are not writing a check. The policy is paying for itself.

Nice trick.

Until it is not.

Cash value can start getting consumed faster than the policy earns interest or dividends. A policy that once looked self-sustaining begins sliding into a slow drain.

The policy does not send a dramatic letter saying, “We are now eating your asset.”

It just does it politely.

The Original Need May Be Gone

Most people did not buy life insurance because they were bored. They bought it because somebody depended on them.

A spouse needed protection. Children were young. A mortgage was large. A business needed continuity. There was a real obligation on the table.

But life changes.

By 60 or beyond, many people discover the original emergency has quietly retired. The mortgage may be paid off. The children may be independent. Retirement accounts may be built. Business obligations may have ended. A surviving spouse may have sufficient assets and income.

In that situation, keeping a large life insurance policy can become less about protection and more about habit.

Habit is expensive.

A policy that made perfect sense at 42 may make very little sense at 67. That does not mean the original decision was wrong. It means the job changed. Good planning is not loyalty to old paperwork.

Cash Value Is Still Capital

Cash value is not imaginary.

If a policy has accumulated substantial value, that money has opportunity cost. Every dollar inside the policy could potentially be used somewhere else.

For a retiree or near-retiree, that may matter more than a death benefit no one truly needs anymore.

Cashing out a policy can free money to increase retirement income, pay off debt, cover healthcare expenses, invest in income-producing assets, build an emergency reserve, or improve quality of life. And yes, quality of life is allowed to count.

There is a strange strain of financial thinking that treats spending money on your actual life as failure, as if the highest calling of capital is to remain trapped in statements until everyone is too tired to enjoy it.

Nonsense.

Money is stored agency. If the policy protects someone who genuinely needs protection, keep analyzing. But if its main function is to shrink quietly while everyone pretends the old plan is sacred, bring the asset back into the room.

The Risk of Waiting Too Long

One ugly outcome is policy collapse.

As insurance costs rise, the policy may reach a point where cash value can no longer support the monthly deductions. Then the owner may be forced to make large premium payments just to keep coverage alive.

That is a miserable position.

The policy that once promised security starts demanding ransom.

If the owner cannot make those payments, the policy may lapse. Depending on loans, gains, and tax basis, that lapse can create unpleasant tax consequences.

This is why waiting can be dangerous. The decision is not simply “keep it or surrender it.” The real decision may be:

Do I take control while meaningful cash value remains, or do I let rising costs make the decision for me later?

One is planning. The other is hoping the machine stays friendly.

Machines rarely do.

Taxes Matter, But They Are Not the Whole Story

Cashing out a permanent life insurance policy can have tax consequences. Generally, if surrender value exceeds total premiums paid, the gain may be taxable as ordinary income.

That matters. It is also not automatically a dealbreaker.

A policyholder should review cost basis, surrender value, outstanding loans, projected charges, and tax impact before deciding. This is not cocktail-napkin math. A qualified tax advisor, insurance professional, or financial advisor should run the numbers.

This article is not financial, tax, legal, or insurance advice. Life insurance is contract-specific, state-specific, and situation-specific. There are exceptions, and some policies should absolutely be kept.

Taxes are part of the calculation. They are not a magic spell that turns a deteriorating policy into a good one.

When Keeping the Policy Still Makes Sense

Cashing out is not always the right move.

Maintaining coverage may still make sense if the death benefit is needed for estate planning, a dependent family member, heir liquidity, or a spouse with limited resources.

Some policies also perform well. Others have tax advantages or legacy purposes that should not be casually discarded.

The point is not that everyone over 60 should surrender life insurance. The point is that everyone over 60 with a cash-value policy should stop assuming the policy deserves automatic renewal in their life.

Assumptions are where money goes to nap.

The Real Question

After 60, financial life becomes less about accumulation and more about alignment.

What still matters? Who still depends on you? What risks are real? What obligations have expired but are still sending invoices?

A life insurance policy with substantial cash value may be one of those assets that needs a fresh look.

If the original need is gone, the cost of insurance is rising, and cash value is being consumed to maintain a death benefit that no longer changes anyone’s life, surrendering the policy may be the more rational choice.

Not dramatic. Not reckless. Just rational.

There comes a point where protecting the future can become a way of neglecting the present.

Enough is not retreat. Enough is command.

And sometimes command means looking at an old policy, thanking it for the job it did, and refusing to let it keep billing you for a life you no longer live.

— Silas North