Part 1 followed the sermon.

Part 2 follows the machinery.

That distinction matters because sermons are built for belief. Machinery is built for throughput. A sermon can say “never sell.” A machine has to pay dividends, satisfy credit investors, defend equity value, keep access to capital, and explain why the old slogan now has a corporate footnote the size of a prospectus.

Vera does not object to machines. Machines are useful. They make coffee, print receipts, and occasionally reveal what the marketing department hoped would remain vibes.

The receipt question is simple:

When Strategy’s machine started answering, did Bitcoiners like the answer — or did they keep hearing the sermon?

THE RESERVE NEEDED A RESERVE.

Start with the fiat part, because irony still deserves a chair.

On December 1, 2025, Strategy announced a $1.44 billion USD Reserve. The company said the reserve was intended to support payments of preferred-stock dividends and interest on outstanding debt. It also said the reserve was initially funded by proceeds from sales of class A common stock under its ATM program.

The Bitcoin company with the fortress Bitcoin balance sheet needed a dollar reserve to support the instruments wrapped around the Bitcoin.

Saylor’s quote was precise:

“Establishing a USD Reserve to complement our BTC Reserve marks the next step in our evolution, and we believe it will better position us to navigate short-term market volatility while delivering on our vision of being the world’s leading issuer of Digital Credit.”

There is that word again: evolution.

Maybe it is evolution. Maybe it is responsible liquidity management. Maybe a company issuing preferred stock and debt should absolutely maintain a cash reserve. Grown-up balance sheets do not run on conference applause.

But Vera’s job is to compare the brochure to the invoice.

Bitcoin was sold as protection from fiat debasement. Strategy’s capital machine now needed a fiat reserve, funded through common-stock sales, to support preferred dividends and debt service.

That does not make it fraud.

It does make the hard-money costume a little tighter around the shoulders.

THE THIRTY-TWO COINS.

Then came the sale.

During May 26–31, 2026, Strategy sold 32 BTC for about $2.5 million, at an average sale price of $77,135 per BTC, net of fees and expenses. The proceeds were expected to fund distributions on preferred stock. Strategy still held 843,706 BTC as of May 31, 2026.

So, no, this was not Strategy dumping the treasury into the ocean.

That is not the point.

The point is that the old moral language around selling Bitcoin ran into the new corporate need to prove the collateral was usable.

Saylor had already previewed the move on the Q1 2026 earnings call:

“We’ll probably sell some Bitcoin to fund a dividend just to inoculate the market, just to send the message that we did it. Look, the company's fine. The Bitcoin's fine. The industry's fine. The world didn't come to an end.”

The slogan was “never sell.”

The footnote became “unless the capital structure needs a flu shot.”

To be fair — and Vera is nothing if not annoyingly fair when the paperwork requires it — Saylor’s personal advocacy statements are not corporate covenants. “Never sell your Bitcoin” is not the same document as an SEC filing.

But that is exactly why the question matters.

Did Bitcoiners hear a personal discipline mantra?

A corporate promise?

A religious commandment?

A meme?

Or a marketing atmosphere that made Strategy’s later machine easier to defend?

THE BTC PRAGUE RECEIPT.

The cleanest answer came in the June 2026 BTC Prague interview.

Saylor did not hide the distinction. He explained it.

He said:

“I got very very famous for saying you do not sell your Bitcoin to the plebs… that’s advice to individual retail investors and that is not the way you would run a Bitcoin finance company that actually exists to buy, sell, and pay dividends on Bitcoin.”

There it is.

Do not sell your Bitcoin: advice to individual retail investors.

Strategy: a Bitcoin finance company that exists to buy, sell, and pay dividends on Bitcoin.

That sentence should have landed like a filing cabinet falling down the stairs.

Because it reframes the whole story. The “never sell” line was not a universal law. It was segmented advice. The company was never promising to behave like the pleb. The company was building a machine the pleb could cheer, buy, defend, misunderstand, or finance — but not run.

Maybe that is obvious to capital-markets people.

Fine. Vera has met capital-markets people. They often believe “obvious” means “hidden in paragraph seven with a defined term.”

THE BITCOIN RESERVE BANK.

In the same interview, Saylor called Strategy:

“a Bitcoin reserve bank.”

He explained the structure as equity capital owning Bitcoin, then issuing credit against it.

He also said:

“The company’s entire existence, the whole point of the company is to create Bitcoin backed credit.”

That is not a stray phrase. That is a business model standing upright in daylight.

If Bitcoin was supposed to obsolete central banking, Vera is allowed to ask why Bitcoiners are cheering the construction of a Bitcoin reserve bank.

The answer may be: because it raises Bitcoin’s price.

That is an answer.

It is not the same as the old answer.

The old answer was sovereignty, scarcity, proof, self-custody, hard money, and exit from the credit machine.

The new answer sounds more like: credit markets are enormous, institutions need wrappers, volatility must be managed, and Bitcoin needs structured products to absorb world capital.

Again, maybe true.

Also: different.

THE HORNETS AND THE TROLLS.

Saylor once mythologized Bitcoin’s online immune system as a swarm of cyber hornets:

“#Bitcoin is a swarm of cyber hornets serving the goddess of wisdom, feeding on the fire of truth…”

It was one of the great Bitcoin memes: aggressive, encrypted, righteous, self-defending.

Then some of those same online instincts turned toward Strategy’s capital structure.

In the BTC Prague interview, Saylor referred to critics as “Twitter trolls,” “pundits on X,” and, in one line, “a simplistic troll” who would say selling Bitcoin is bad.

Maybe some critics were trolls. The internet is not exactly a faculty lounge.

But Vera’s question is narrower:

When the swarm attacked Bitcoin’s enemies, it was mythic. When the swarm questioned Strategy’s machine, did it become noise?

That is not a gotcha. That is incentive analysis with a red pen.

A movement’s immune system is always celebrated until it recognizes the wrong cell.

THE COLLATERAL MUST BE SALEABLE.

Here is where the machine speaks most clearly.

Saylor argued that credit investors need to believe Strategy would sell Bitcoin if necessary. If they believe the company would never sell it, he said, then the Bitcoin is not useful collateral.

His words:

“If the credit investors… believe you would never sell it, then you have zero dollars in assets and you have zero dollars in collateral…”

And then:

“The only way that the bitcoin is a tangible asset is if you're willing to sell it.”

That is a remarkable sentence.

To the Bitcoiner, Bitcoin is tangible because of proof, scarcity, private keys, settlement, and the chain.

To the credit investor, in Saylor’s telling, Bitcoin is tangible because Strategy will sell it if the structure requires it.

Same asset. Different altar.

That is the whole story in miniature.

THE MACHINE WORKING PROPERLY.

Saylor then gave Vera the phrase that should sit near the center of the article:

“A simplistic troll would say selling Bitcoin is bad. But the truth is if the selling of the Bitcoin creates equity value and improves creditworthiness then that allows us to sell billions of dollars of credit and that causes the equity to trade up by billions of dollars and that allows us to raise billions in the equity market and then allows us to buy billions of Bitcoin. So in fact the machine working properly and rationally is good for Bitcoin. It’s good for the credit STRC and it’s good for the equity.”

The machine working properly.

Not the wallet.

Not the node.

Not the cold storage.

The machine.

And the machine has a logic: sell when rational, improve creditworthiness, sell more credit, support equity, raise more capital, buy more Bitcoin.

That can be a flywheel.

It can also be a dependency stack.

Vera does not need to choose the word yet. She only needs to ask who feeds the machine, who owns the machine, and who gets fed by it.

THE GUARDRAIL THAT MOVED.

Now to mNAV, because apparently no financial story is complete until someone invents a metric that requires a glossary and a priest.

On July 31, 2025, Strategy told investors it would not issue common equity below 2.5x mNAV except to pay debt interest or fund preferred dividends.

That sounded like a guardrail.

On August 18, 2025, Strategy updated the guidance. Below 2.5x mNAV, it could also issue MSTR when “otherwise deemed advantageous to the company.”

That sounded less like a guardrail and more like a traffic cone with management discretion.

Days later, according to Blockspace, Strategy sold 875,301 MSTR shares through its ATM program between August 18 and August 24, raising about $309.9 million, while Strategy’s dashboard reportedly showed mNAV at 1.65x.

Again, Vera is not calling that illegal.

Vera is asking what the original sentence was for.

If the policy was “we will not issue below 2.5x except for these two cases,” and then the policy became “also when advantageous,” shareholders are entitled to ask whether the number was a discipline rule or a confidence product.

In July, the line was a guardrail.

In August, it became a speed bump with a management-discretion bypass lane.

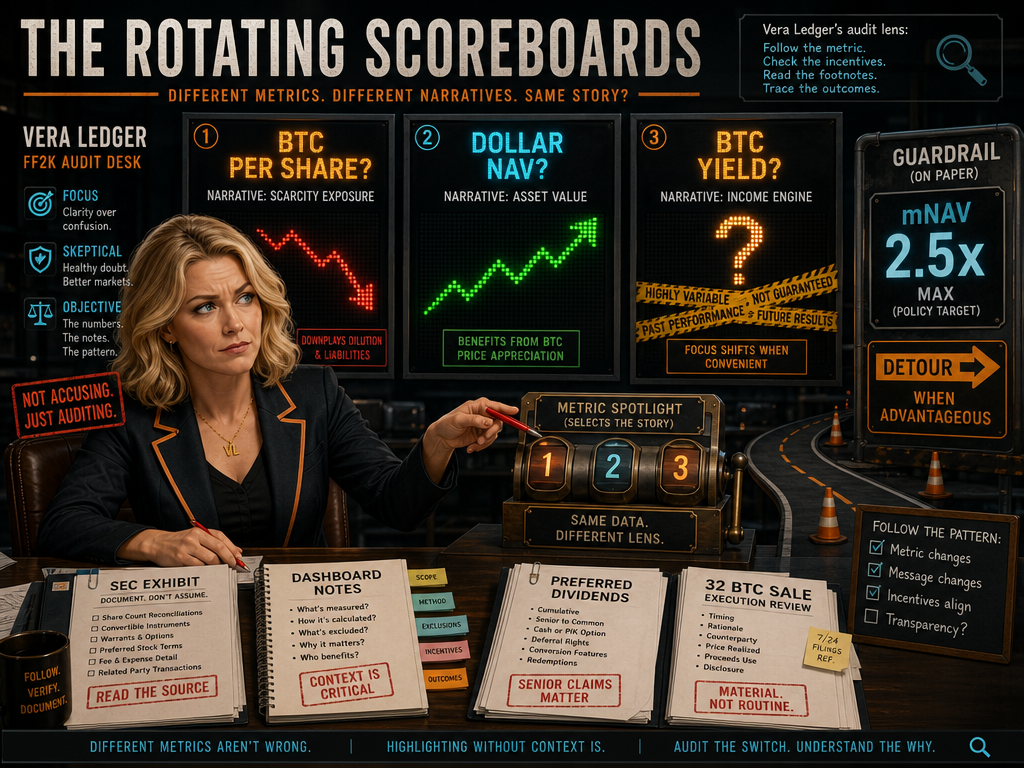

THE ROTATING SCOREBOARDS.

Then came the argument over dilution.

Saylor has argued that investors can calculate Strategy’s mNAV using common equity, preferred equity, and convertible debt, and that gross assets per share and net assets per share are also valid valuation frameworks. He has also argued that issuing equity for cash or Bitcoin is not inherently dilutive because shareholders receive tangible assets in return.

In the BTC Prague interview, he acknowledged the frame shift directly:

“It’s accretive to the equity on a US dollar basis. It’s slightly dilutive on a Bitcoin per share basis.”

That is the sentence.

A transaction can be dilutive on Bitcoin per share and accretive on dollar NAV.

Different metric. Different story.

That does not mean every metric is fake. It means the metric choice matters because the metric chooses the narrative.

BTC per share tells one story.

Dollar NAV tells another.

BTC Yield tells another, and Strategy’s own notes say BTC Yield is not traditional yield and is not a measure of shareholder investment return, income, operating performance, ROI, or traditional yield.

So when the scoreboard changes, Vera asks who changed it, why, and who was losing on the old one.

Different metrics are not automatically wrong.

Highlighting one without context is how the magician tells you to watch the left hand.

THE PSYCHOLOGICAL PIVOT.

Near the end of the BTC Prague interview, Saylor said the fundamentalist ideology is important to Bitcoin’s soul, but taken too far it locks out 99.9% of world capital.

He also said if you ask 100 people whether they would rather have volatile Bitcoin exposure or a bank account paying 10% with no stress and no volatility, 99 out of 100 would take the low-stress bank account.

Then he added:

“We know this for certain. We’ve actually run the focus groups.”

That may be the most revealing line in the whole file.

Bitcoiners were taught to endure volatility because volatility was the price of the escape.

Strategy now knows most people do not want the escape raw. They want the yield wrapper. They want low stress. They want the bank-account feeling with Bitcoin collateral glowing somewhere in the basement.

That is not moral failure. It is product-market fit.

But call it what it is.

Digital Credit is not just Bitcoin education. It is a product architecture designed around the fact that most people do not want Bitcoin’s defining discomfort.

THE $20 MILLION CONDITION.

Saylor’s big-picture defense is also clear.

He argued that if Bitcoin is going to reach $20 million, capital must flow from the credit markets. He said Bitcoin reached $100,000 because capital came from ETFs, Strategy, and other institutional sources, and without that flow Bitcoin would be trading far lower.

This is the bridge thesis.

Bitcoin cannot win at global scale, he argues, by rejecting nation states, currencies, governments, bonds, equities, credit instruments, money managers, and funds. It has to engage them.

That may be right.

It may also be the exact moment the revolution starts leasing office space in the old regime.

Vera’s question is not whether credit-market capital can raise the price of Bitcoin.

The question is whether Bitcoiners understand what has to be built, promised, sold, diluted, renamed, defended, and occasionally liquidated to invite that capital in.

THE LEDGER READ.

This is the cleanest version of the thesis:

Saylor did not necessarily hide the machine.

He may have said it plainly enough for anyone willing to hear the second half of the sentence.

The problem is that Bitcoiners fell in love with the first half.

They heard: digital gold.

They heard: no second best.

They heard: volatility is vitality.

They heard: never sell.

They heard: cyber hornets.

Then Strategy built a Bitcoin reserve bank, issued Digital Credit, engineered price stability, created a USD reserve, sold Bitcoin to fund preferred distributions, told credit investors the collateral was real because it could be sold, widened the mNAV guardrail, and described critics as trolls.

Maybe that is brilliant.

Maybe that is necessary.

Maybe it is exactly how Bitcoin enters the world’s balance sheets.

But nobody should pretend it is the same story.

STAMP.

Final stamp: not proven fraud, not simple betrayal, and definitely not the old sermon.

The receipts show a more uncomfortable possibility.

Bitcoiners may not have been bamboozled because Saylor lied.

They may have been bamboozled because he told them what he was building, and they only heard the parts that sounded like church.

The machine answered.

The crowd is still deciding whether it heard music or gears.

- Vera Ledger