The first move is always the frame.

Not the ticker. Not the preferred-stock alphabet soup. Not the polished explanation for why selling 32 Bitcoin is actually discipline, liquidity, transparency, and a master class in chess-not-checkers capital markets.

The frame.

That is what matters in Episode 60 of The Hurdle Rate. The useful part is not that a room full of Bitcoin treasury insiders believes Bitcoin-linked financial engineering is misunderstood. Of course they do. Every product desk in history has believed the public would love the structure if only the public were smarter, calmer, and less attached to boring questions like: why not just buy the thing underneath it?

Bitcoin used to have a beautifully clean pitch.

Buy the asset. Hold the asset. Stop volunteering for the room where financial engineers keep adding doors, wrappers, fees, maturities, covenants, distribution policies, and acronyms until the ordinary buyer needs a translator and a sedative.

Now the sermon comes with preferred shares.

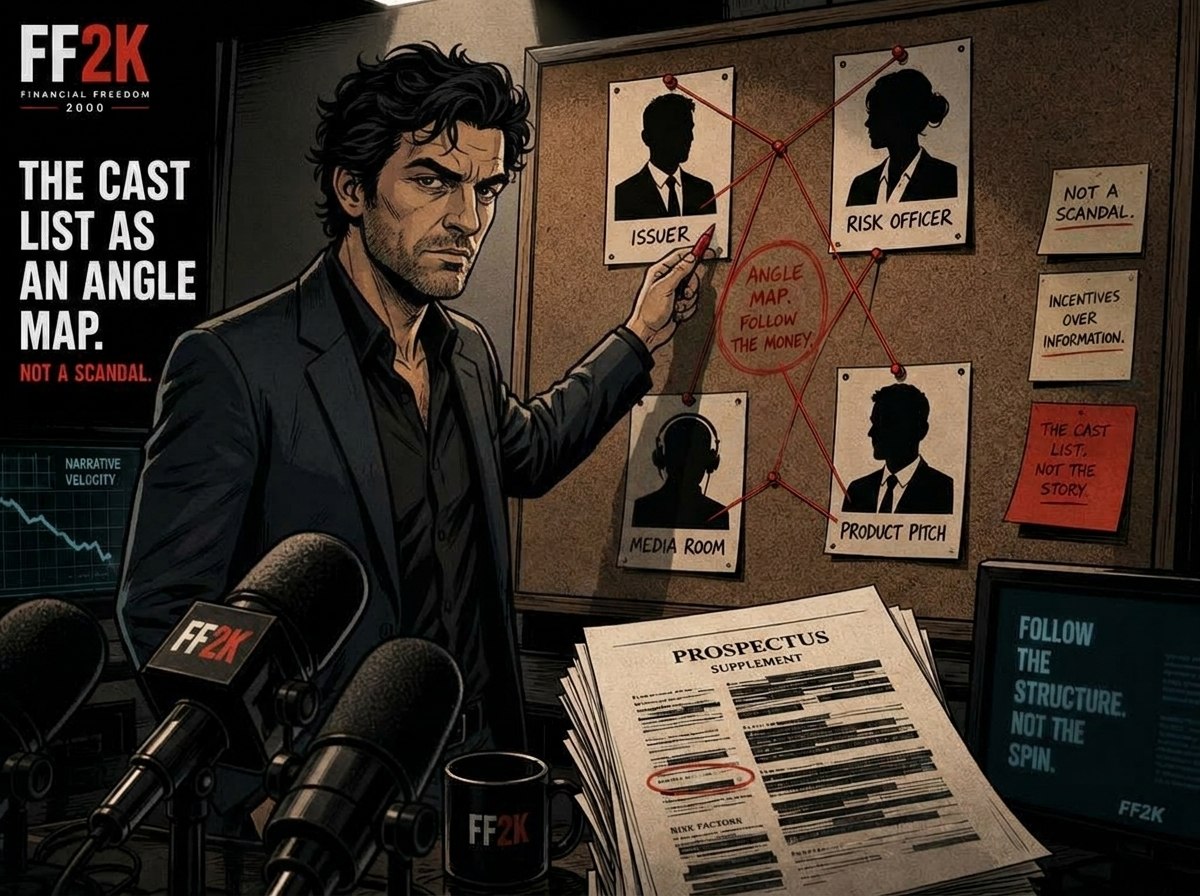

The cast list matters. Matt Cole is Strive’s CEO. Jeff Walton is Strive’s Chief Risk Officer and the founder/CEO of True North, a Strive subsidiary built around Bitcoin treasury adoption, securitization, collateralized finance, and macro strategy. Ben Werkman is Strive’s Chief Investment Officer. Tim Kotzman operates inside the Bitcoin treasury media ecosystem. None of that is a scandal. It is the angle map.

When that room talks about ASST, SATA, amplification ratios, dividend reserves, daily dividends, digital credit, Strategy preferreds, and why critics do not understand the math, the audience deserves to know who benefits if the room wins the frame.

The frame goes like this:

Strategy sells 32 BTC, but only unserious critics think that matters.

Saylor still understands the game.

Strive is scaling.

Preferred instruments are evolving.

Daily dividends are psychologically powerful.

Amplification is not danger; it is optimized exposure.

Digital credit is not complexity; it is category creation.

Watch the steering wheel.

The basic retail question is still sitting there with its hand up: why not just buy Bitcoin?

The episode turns that question into a status test. If you ask it, maybe you are unsophisticated. Maybe you do not understand credit. Maybe you do not understand reserves. Maybe you cannot read a balance sheet. Maybe you are one of those people running around with your head cut off because 32 BTC moved from one column to another.

That is a beautiful trick. Not because it proves the structure works. Because it moves the burden.

Instead of the issuer explaining why a public buyer should prefer a Bitcoin-linked security over Bitcoin itself, the skeptic now has to prove he is smart enough to be allowed in the conversation.

That is how product complexity borrows Bitcoin’s moral clarity.

Bitcoin is hard money. Preferred shares are paperwork. Bitcoin has no boardroom. These instruments have executives, filings, dividend policies, capital-market assumptions, reserve math, investor psychology, return-of-capital tax treatment, seniority risk, dilution dynamics, and market confidence loops.

Bitcoin does not need daily dividends to feel real. A product with issuer credit risk does.

That does not automatically make the product bad. It makes the pitch different.

And different is where the public gets lost.

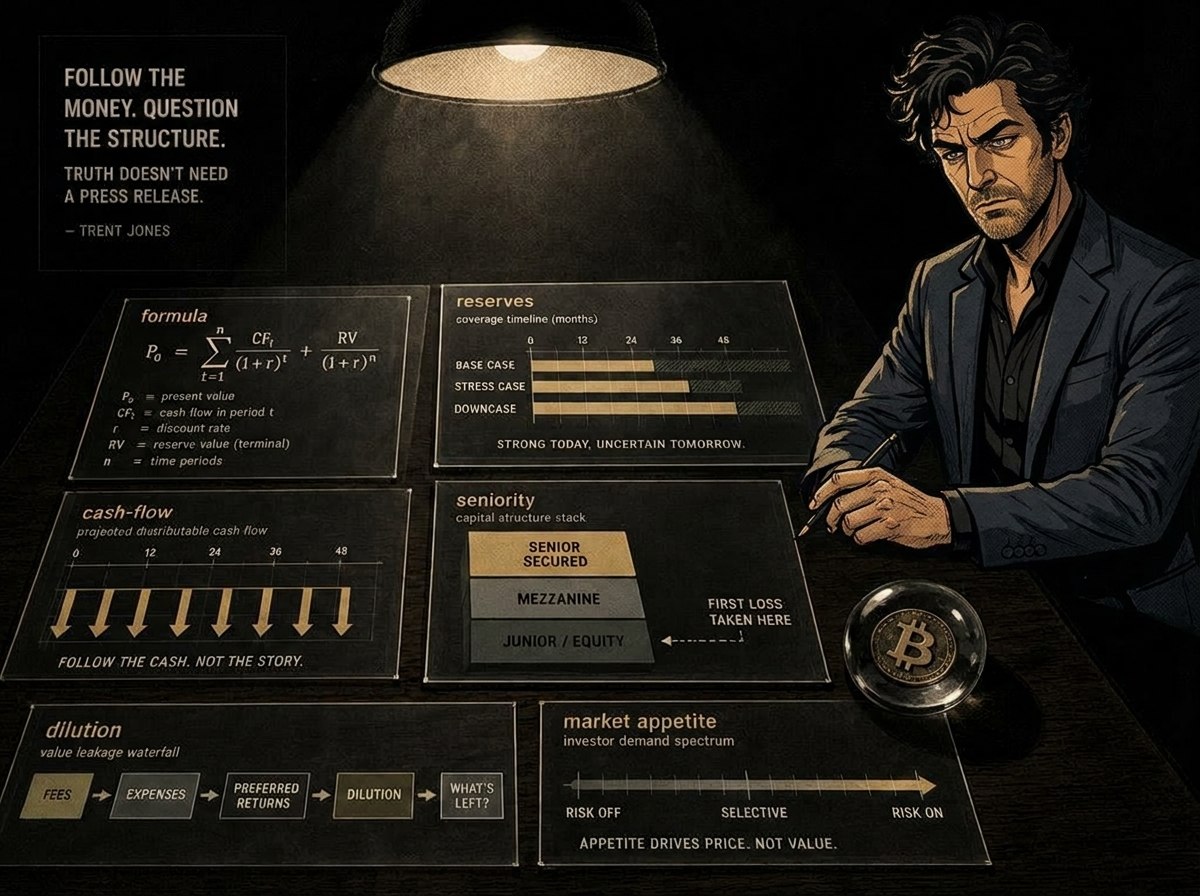

The room talks about stress tests, par ranges, capital raised per day, reserve coverage, bear-market duration, and how to manage supply around a $100 stated amount. Fine. Those are real topics. Serious people should ask serious questions about them.

But the ordinary listener hears something softer:

You are early. They are stupid. The math is on our side. The future has a ticker.

The words do a lot of work. “Par” makes price feel anchored. “Reserve” makes payments feel protected. “Yield” makes cash feel earned. “Return of capital” makes the tax pitch sound civilized. “Digital credit” makes old machinery sound like it got a software update.

But a new label does not cancel the old questions.

What has to keep working?

The issuer. The asset price. The board. The dividend policy. The market’s appetite. The next financing window. The confidence loop. The willingness of investors to keep treating the preferred near par. The belief that a Bitcoin treasury company can turn volatility into something credit-like without smuggling the volatility back in through another door.

If the answer requires all of that, say so.

Because this is not just Bitcoin with better manners. It is a capital structure. And capital structures have angles.

The Hurdle Rate panel may be right that the critics are missing pieces of the model. Maybe the reserve math is better than the skeptics think. Maybe the preferreds are more durable than the one-line dunkers understand. Maybe the common-stock pain and preferred-stock behavior need to be separated cleanly.

Good. Then put the model on the desk.

Show the formula. Show the reserve definition. Show where the cash comes from. Show what happens after the reserve window. Show who is senior, who is junior, who has discretion, and who gets diluted when the market stops clapping.

Until then, the public is allowed to notice the oldest sales maneuver in finance:

Make the product sound sophisticated. Make the skeptic sound dumb. Move the burden before the receipt hits the table.

Everybody has an angle.

This one brought a prospectus.

- Trent Jones