The first move is the chart.

Not the filing. Not the share count. Not the little trapdoor under the word “yield.” The chart.

Michael Saylor posts the orange dots, and the dots do what orange dots are hired to do. They imply discipline. They imply inevitability. They imply that Strategy is still doing the only thing the crowd came to watch: buying more Bitcoin while everybody else loses nerve.

The dots are real. Strategy bought more Bitcoin. On June 8, the company reported selling 1,409,600 shares of Class A common stock for about $181 million in net proceeds, buying 1,550 BTC for about $101.3 million, and rebuilding a $1 billion U.S. dollar reserve for preferred dividends and debt interest. Those are not vibes. Those are receipts.

But a receipt is not a verdict.

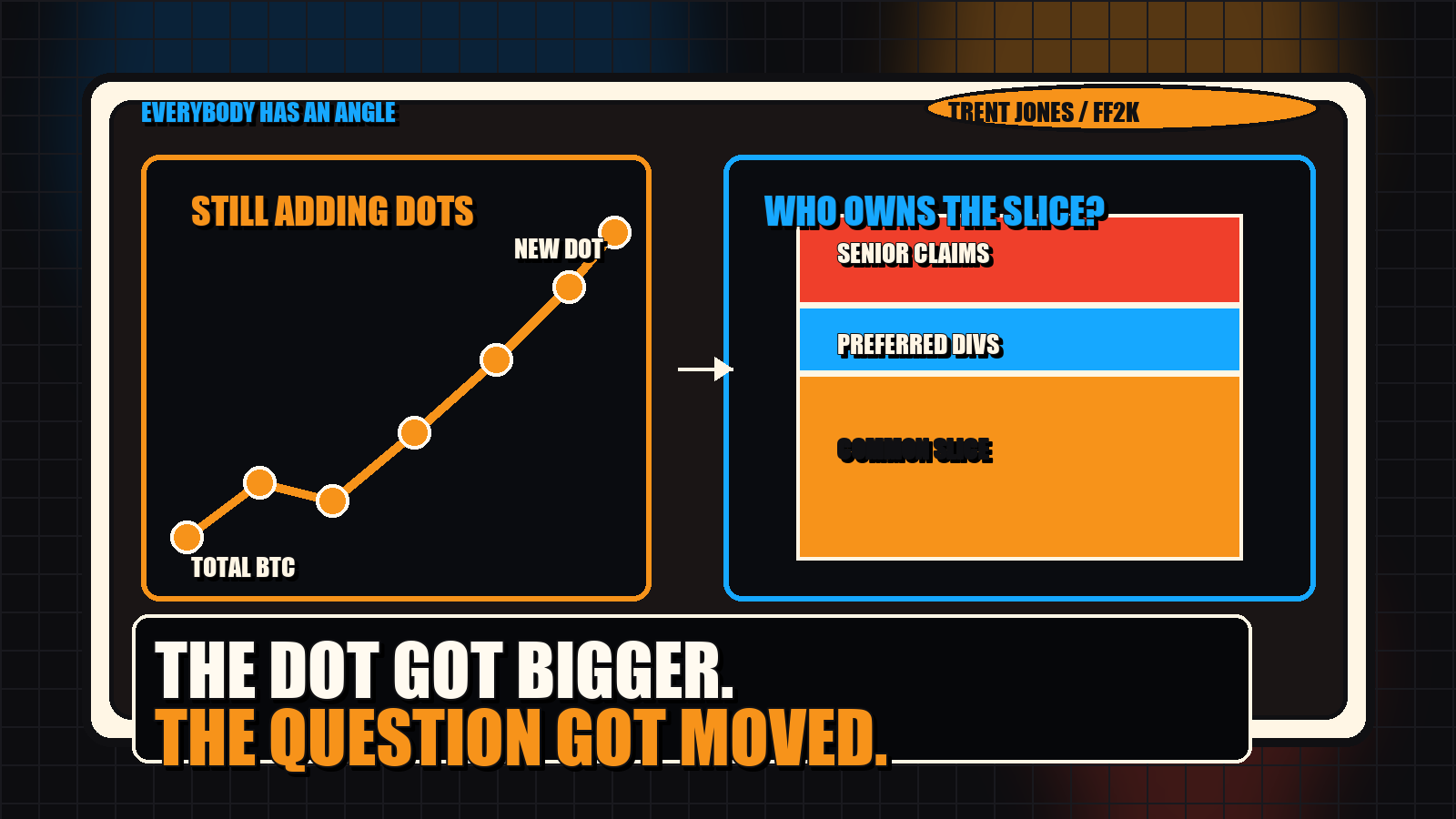

The question is not whether the pile got bigger. The question is who paid for the new dot, what claim sits ahead of common, and whether the common holder’s actual slice improved after the paperwork finished doing its little dance in the conference room.

That is why Saylor’s new language matters. He says BPS measures Bitcoin per common share before senior claims. CEBE BPS measures Bitcoin per common share after senior claims. CEBE is the conservative risk metric. BPS is the common equity growth metric. BTC Yield measures BPS execution.

Fine. That distinction is useful.

It is also an admission.

If Bitcoin per share now needs a before-senior-claims number and an after-senior-claims number, then the old simple victory lap was incomplete. Strategy is no longer just “leveraged Bitcoin” with a ticker attached. It is Bitcoin inside a claims waterfall wearing a laser-eye lapel pin.

That does not make it a scam. It makes it a capital structure. Capital structures have doors. Some people stand closer to the exit than others.

The pro-Saylor case has its strongest version, and it is not stupid. Selling common stock is not automatically economic dilution if the company sells at a premium and uses the proceeds to improve common exposure. Critics who stare only at share count can miss the asset side of the trade. Gross BPS, net CEBE BPS, liability duration, preferred claims, and market premium all matter.

That is the adult defense. It deserves to be heard before the internet starts throwing the word Ponzi around like a drunk with a confetti cannon.

But the defense has a problem: it concedes the thing it is trying to soften.

The product got more complicated because the machine got more complicated. Common equity, preferred stock, converts, cash reserves, dividend obligations, ATM issuance, Bitcoin price volatility, market appetite, and mNAV premium are now part of the story. Once those things enter the room, the chart is not enough. The orange dot is a headline. The cap table is the article.

The counterargument is not anti-Bitcoin. It is pro-scoreboard.

CryptoKaleo asked the clean version: where does the money for the yield come from? If operating revenue is not the engine, then the cash has to come from somewhere — common issuance, preferred issuance, debt, cash reserve, or Bitcoin sales. Each path has a cost. Each path changes who carries risk.

SumOfAllGainz made the retail version: you sold a lot of paper, bought some coins, and parked the rest in reserve. Maybe that is prudent. Maybe it is necessary. But do not ask common holders to clap only at the coin purchase and ignore the claim dilution and reserve funding that made the purchase possible.

DeFi Andree had the sanest middle: selling equity looks like dilution, selling BTC looks like breaking the promise, and the real test is whether BTC per share improves over time. That is the right test because common holders do not eat total Bitcoin. They eat their slice.

Then there is the sharper governance complaint: if public Class A holders absorb ATM dilution while insiders retain control through class structure, the word “alignment” deserves a flashlight. That claim needs careful proving before anyone uses it like a hammer, but the question belongs on the board.

Saylor’s side wants the conversation on amplification: the company can issue capital, acquire Bitcoin, and let Bitcoin’s long-term rise outrun the cost of the capital stack. If that works, common gets a leveraged claim on a growing pile. If BTC runs, the model looks less like dilution and more like financial judo.

The critics want the conversation on burden: if the stock is down, the ATM is open, preferred obligations exist, and part of the raise rebuilds cash instead of buying Bitcoin, then common holders deserve a net-common scoreboard, not just a bigger total-holdings graphic.

That is the whole fight.

BPS is the theater marquee. CEBE is the fire-exit map.

Saylor introducing CEBE does not kill the thesis. It makes the thesis more honest. But it also moves the frame. The old crowd-friendly question was “How much Bitcoin does Strategy own?” The better question is “How much Bitcoin exposure is left for common after the senior claims, financing costs, reserves, and future issuance are done taking their seats?”

That second question is less fun. It does not fit as neatly under an orange dot. It also happens to be the question common holders are actually paying for.

Everybody has an angle.

This one brought two metrics and a very pretty chart.

- Trent Jones