The first move was not the Bitcoin purchase.

It was the cast list.

Public Bitcoin treasury companies have discovered something every old-media producer already knew: if you want the audience to trust the product, put a familiar face near the microphone.

The face does not have to run accounting. It does not have to negotiate the convertible note. It does not even have to sit in the office every day. It has to make the room feel Bitcoin-native before the prospectus starts speaking fluent capital structure.

That is the new angle inside the Bitcoin treasury boom.

The companies are not only stacking sats.

They are stacking reputations.

Stephan Livera is listed as an investor/advisor to OranjeBTC. Pierre Rochard is on Strive’s board while running The Bitcoin Bond Company. Preston Pysh joined BitcoinTreasuries.net as a strategic advisor. Dylan LeClair went from Bitcoin research to Metaplanet’s Bitcoin strategy seat. Mark Moss became Chief Bitcoin Strategist at Satsuma. Semler added Natalie Brunell to its board and hired Joe Burnett as Director of Bitcoin Strategy. Saifedean Ammous became a board advisor to Genius Group. Eric Weiss, Saylor’s orange-pill origin story in human form, appears in Murano, BitcoinTreasuries.net, and other treasury-company orbitals. David Bailey built Nakamoto. Adam Back is attached to BSTR. Anthony Pompliano built ProCap BTC into a public-market Bitcoin finance vehicle through a SPAC combination.

That is not random.

That is a market structure learning how to wear a culture.

The public story

The public story is simple: Bitcoin companies are hiring Bitcoin people.

Fine. Sometimes that is exactly true.

A Bitcoin treasury company should probably include people who understand Bitcoin better than a regional bank director who still calls it “the blockchain.” A board supervising a Bitcoin balance sheet should know the difference between custody, treasury policy, issuance, shareholder dilution, BTC yield, Bitcoin per share, mNAV, preferred claims, and retail investor psychology. A company selling Bitcoin-linked securities needs people who can explain the machine without accidentally summoning a securities lawyer through the air vent.

That is the adult version.

But the adult version is not the whole version.

Because these companies are not merely hiring expertise. They are hiring translation. They are hiring borrowed trust. They are hiring a pre-warmed audience.

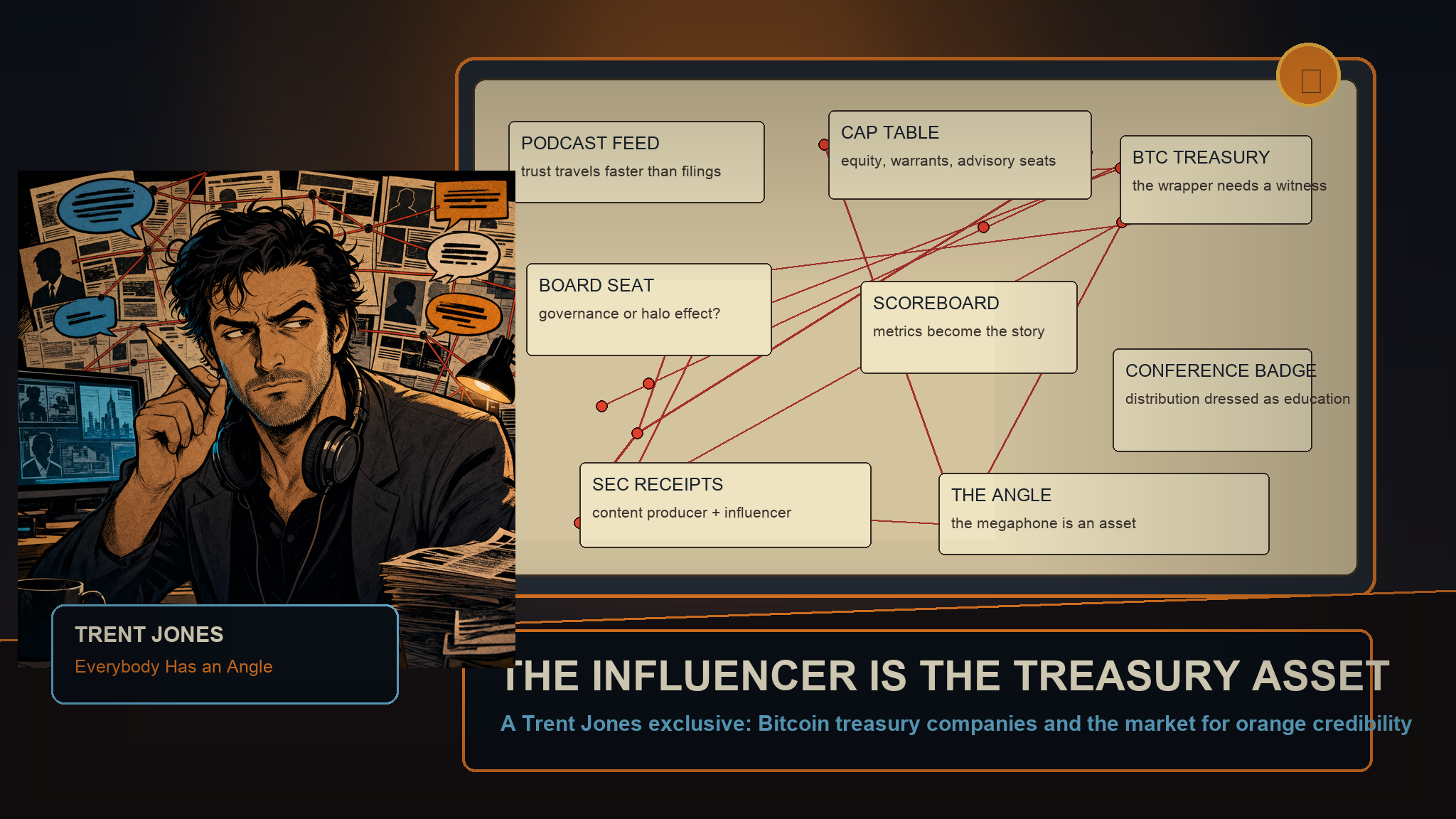

The influencer is not adjacent to the asset.

In this market, the influencer helps make the wrapper legible.

The cast list

Start with the cleanest receipt.

Semler Scientific’s proxy says the quiet part in public-company English. Semler tells shareholders it has strengthened its Bitcoin team and its “connection to the Bitcoin community.” It says it added Natalie Brunell, “a highly regarded Bitcoin advocate and content producer,” to the board. Then it says it hired Joe Burnett, “another leading voice and influencer in the Bitcoin community,” as director of Bitcoin strategy.

That is one paragraph doing a lot of work.

The company does not hide the word influencer. It puts it in the filing.

Watch the sequence:

- strengthened Bitcoin team;

- strengthened connection to the Bitcoin community;

- added advocate and content producer to the board;

- hired leading voice and influencer as strategy director;

- stockholder base grew.

No one needs to invent a conspiracy when the filing hands you the choreography.

The board seat is credibility. The strategy title is authority. The community connection is distribution. The larger shareholder base is the business case sitting politely at the end of the sentence.

Now widen the frame.

**Stephan Livera** appears as Investor/Advisor, OranjeBTC, on a Bitcoin for Corporations speaker page. That label tells Bitcoiners two things at once: he has economic exposure, and he looked at the thing closely enough to attach his name. The audience hears: one of ours is in the room.

**Pierre Rochard** sits on Strive’s board, while also serving as CEO of The Bitcoin Bond Company. Strive’s announcement frames the board as stacked with experienced Bitcoin executives. That is not just governance. It is a credibility stack. If Strive wants the market to see a public asset-management company as a Bitcoin treasury vehicle, Pierre’s presence tells the audience: this is not tourist Bitcoin.

**Preston Pysh** is one level away from the issuer, which may be more interesting. BitcoinTreasuries.net appointed him strategic advisor to help evaluate Bitcoin companies. That is not an operating role inside a DAT. It is scoreboard power. In a market full of treasury companies, the dashboard becomes a judge. The metrics become the language. The language becomes the trade.

**Dylan LeClair** went from Bitcoin research and media into Metaplanet’s Bitcoin strategy role. This is the researcher-to-operator path. He had already built public credibility around treasury-company analysis. Then a treasury company hired him to help run the thesis.

**Mark Moss** is the megaphone hire with the least disguise. Satsuma’s London Stock Exchange announcement cites his YouTube audience, his X following, his educational output, and his Bitcoin treasury work. That is not subtle. That is an issuer saying reach is part of the résumé.

**Saifedean Ammous** became board advisor to Genius Group as the company pursued a Bitcoin treasury and Bitcoin-first products. The Bitcoin Standard brand becomes institutional seasoning. Put his name near the treasury plan and the audience knows what worldview is being imported.

**Eric Weiss** brings a different asset: origin-story credibility. He is widely associated with helping introduce Michael Saylor to Bitcoin. When BitcoinTreasuries.net brings him in as strategic advisor, or when filings and announcements place him around treasury vehicles, the message is not hard to read. Saylor’s mentor is now near the scoreboard.

**David Bailey** and **Anthony Pompliano** are the founder-route version of the same pattern. They are not influencers sprinkled onto someone else’s company. Their media, investor, and Bitcoin-native reputations become part of the company’s formation story.

The cap table has a podcast now.

The network map

The recurring nodes are not hard to find.

BTC Inc. Bitcoin Magazine. UTXO Management. Swan alumni. Bitcoin for Corporations. Strategy/Saylor-adjacent events. BitcoinTreasuries.net. Strive. Metaplanet. OranjeBTC. Nakamoto. Semler. Satsuma. ProCap. BSTR.

Different companies. Different structures. Different jurisdictions. Different levels of seriousness.

Same need.

A Bitcoin treasury wrapper has to answer the question the market keeps asking under its breath:

Why not just buy Bitcoin?

The answer is never only mathematical.

It is also narrative.

Maybe the company has a capital-market advantage. Maybe it can issue at a premium. Maybe it can use convertibles. Maybe it can acquire Bitcoin faster than the common shareholder could alone. Maybe it can get index inclusion, institutional flows, tax advantages, or financing access. Maybe it can build Bitcoin-backed financial services. Maybe it can turn the public-market wrapper into something genuinely accretive.

Maybe.

But the wrapper still needs the crowd to believe.

That is where the cast list earns its keep.

A familiar podcaster reduces suspicion. A respected researcher translates complexity. A board advisor imports ideology. A data-site advisor helps shape the scoreboard. A conference network supplies rooms full of prospective believers. A founder with a media machine turns attention into deal flow.

The public calls it education.

The market may call it distribution.

The reader can decide how far apart those words really are.

The routes into the room

There are five paths.

1. Research analyst to operator

Dylan LeClair and Joe Burnett are the cleanest examples.

They analyzed the treasury-company model publicly, built credibility around the thesis, then moved into companies executing the thesis. This is not inherently suspicious. It is also not neutral. The analyst becomes part of the system he had been explaining.

That changes the frame.

The old role was: here is how the machine works.

The new role is: here is why our machine works.

2. Audience to strategist

Mark Moss fits here. So does part of the Stephan Livera story.

This path says distribution matters. The résumé is not just “knows Bitcoin.” It is “can bring Bitcoiners with him.” That can be useful for investor education, brand legitimacy, shareholder growth, conference appearances, podcast reach, and defending the company’s narrative when the market gets ugly.

A treasury company with a weak community connection has to buy attention.

A treasury company with the right adviser can borrow it.

3. Board/advisor credibility

Natalie Brunell, Pierre Rochard, Saifedean Ammous, Eric Weiss.

These names do not all mean the same thing. One is media credibility. One is capital-markets Bitcoin credibility. One is ideological authority. One is institutional adoption lore.

But the function rhymes.

They signal to a Bitcoin audience that the company is not merely wearing orange for the investor deck.

4. Scoreboard control

Preston Pysh and Eric Weiss at BitcoinTreasuries.net sit in the measurement layer.

This is the layer people ignore until it starts deciding who wins.

If Bitcoin treasury companies become a category, the category needs rankings, ratios, dashboards, vocabulary, and league tables. Once that happens, the scoreboard is not just a mirror. It is a steering wheel.

What counts as success?

Total BTC? BTC per share? BTC yield? mNAV? Debt coverage? Preferred obligations? Common dilution? Operating cash flow? Geographic arbitrage? Founder alignment?

The metrics are not boring.

The metrics are the argument.

5. Founder route

David Bailey. Anthony Pompliano. Adam Back.

This is where reputation does not advise the vehicle. Reputation becomes the vehicle.

The founder route turns a media/investor/Bitcoin-native audience into a financing surface. The pitch is no longer “trust this company because respected Bitcoiners are nearby.” It becomes “trust this company because the respected Bitcoiner built it.”

That is cleaner.

It is also more direct.

The missing scene

The missing scene is compensation.

Who got equity? Who got warrants? Who invested in the PIPE? Who received director stock? Who has lockups? Who receives cash advisory fees? Who gets performance equity? Who owns related entities? Who is advising more than one treasury vehicle? Who appears on podcasts without the audience knowing the full economic relationship?

Some of that will be in filings.

Some will be buried in footnotes.

Some will not be public at all.

That is why the map matters before the verdict.

Do not start with accusation. Start with inventory.

Observed: public Bitcoin treasury companies and treasury-market infrastructure firms are placing Bitcoin podcasters, researchers, educators, conference figures, authors, media operators, investor-influencers, and Saylor-adjacent credibility figures into board, advisory, strategy, data, and founder roles.

Observed: official announcements and filings repeatedly describe these figures in terms of community connection, content production, influence, audience, education, Bitcoin credibility, and capital-market strategy.

Observed: the same network nodes recur: BTC Inc., Bitcoin Magazine, UTXO, Swan, Bitcoin for Corporations, Strategy-adjacent events, BitcoinTreasuries.net, Strive, Metaplanet, Nakamoto, Semler, Satsuma, ProCap, BSTR.

Inference: the public-market Bitcoin treasury category is not only competing for capital. It is competing for cultural legitimacy.

Open question: who is paid when legitimacy converts into financing?

The compensation layer

The table below uses a stricter rule than the usual review-source shuffle. A filing counts. An issuer prospectus counts. An SEC exhibit counts. A company’s own role announcement can identify a role. Ten articles copying the same press release do not become ten sources just because they wore different ads around the paragraph.

So the visible pattern has two columns: what the public record exposes, and what it does not.

| Person | Company / vehicle | Public role | Compensation visible in primary records | Primary receipt |

|---|---|---|---|---|

| David Bailey / BTC Consulting LLC | KindlyMD / Nakamoto | Designated individual under consulting agreement; founder/CEO/chairman route | $58,333.33 monthly fee; target cash incentive up to $2.1M; 5,000,000 stock options; initial RSU grant value $1M; $250k signing bonus; possible private aircraft travel and expenses. | SEC Exhibit 10.15 |

| Anthony Pompliano | ProCap BTC / ProCap Financial | Founder / CEO | $1 salary; 100% of personal equity compensation tied to “moonshot” stock-price milestones. Equity begins vesting at $15/share and continues in $2.50 increments through $50/share. Board equity begins at $12.50/share and runs through $20/share. | SEC Exhibit 99.1 |

| Natalie Brunell | Semler Scientific | Board director; Bitcoin advocate / content producer | Exact 2025 individual amount not yet in the 2024 table. Semler discloses she joined in May 2025, received no 2024 compensation, and falls under a non-employee director framework: $45k annual board retainer, committee retainers, annual equity, and pro-rata equity awards for mid-cycle directors. | Semler DEF 14A |

| Joe Burnett | Semler Scientific | Director of Bitcoin Strategy | Compensation not found in the current public proxy excerpt. The same filing names him as a “leading voice and influencer” hired as Director of Bitcoin Strategy. | Semler DEF 14A |

| Pierre Rochard | Strive | Director | Director role confirmed; compensation sections exist in the Form 10-K. Individual director table still needs exact row extraction before assigning a dollar value. | Strive 2025 Form 10-K |

| Mark Moss | Satsuma Technology PLC | Chief Bitcoin Strategist | Role confirmed in issuer prospectus. Exact strategist/advisor remuneration, options, warrants, or related-party economics not extracted yet. | Satsuma prospectus |

| Saifedean Ammous | Genius Group | Board Advisor | Role disclosed in SEC-filed/company materials. No advisor fee, equity grant, or warrant package found in first-pass public filings. | Genius Group SEC exhibit |

| Preston Pysh | BitcoinTreasuries.net | Strategic advisor | No public compensation disclosure found; private/non-reporting scoreboard layer. | Official announcement |

| Stephan Livera | OranjeBTC | Investor / Advisor | No public compensation disclosure found in first pass; marked undisclosed rather than padded with syndicated review copies. | Bitcoin for Corporations profile |

The strongest receipt is Bailey/Nakamoto because the agreement says the numbers out loud. Pompliano’s ProCap filing says the compensation structure out loud. Brunell’s Semler filing gives the board-compensation framework and the timing problem: she joined in 2025, so the 2024 table does not yet show her individual total. Burnett is named as an influencer-strategy hire, but the compensation is not disclosed in the proxy. Rochard, Moss, Ammous, Pysh, and Livera show why the blank spaces matter: some roles are public, while the economics remain either pending, buried, private, or undisclosed.

That absence is not proof of wrongdoing.

It is proof that the public can see the influence layer faster than it can see the economics behind the influence layer.

The question under the question

The Bitcoin treasury pitch has one permanent problem.

Bitcoin itself is simple.

The wrapper is not.

Bitcoin has no board. No advisor agreement. No influencer director. No PIPE allocation. No preferred claim. No convertible note. No ATM program. No conference sponsorship. No investor-relations calendar. No dashboard deciding whether this week’s dilution is accretive if you hold the chart at the correct angle and squint like a gentleman.

The wrapper has all of that.

Maybe the wrapper is useful.

Maybe it is clever.

Maybe it gives institutions access they cannot get directly.

Maybe it outperforms.

Maybe it does not.

But the wrapper needs a story because the wrapper adds trust back into an asset famous for removing trusted intermediaries.

That is the quiet irony.

The more financial engineering gets built around Bitcoin, the more the product needs Bitcoiners standing nearby saying: this is still ours.

Not necessarily in those words.

Usually in better lighting.

What the reader can see now

Here is the map without the music:

- The companies buy Bitcoin.

- The companies issue paper.

- The companies need capital-market demand.

- Capital-market demand needs a story.

- The story needs Bitcoin-native credibility.

- Bitcoin-native credibility comes from podcasters, educators, researchers, authors, conference operators, and prior Saylor-network figures.

- Those figures receive titles: board director, strategic advisor, investor/advisor, director of Bitcoin strategy, chief Bitcoin strategist, founder, CEO.

- The audience sees familiar names near unfamiliar structures.

- The unfamiliar structures feel less foreign.

That is the pattern.

No one has to tell the reader what to think about it.

The reader can stare at the pattern and do the math.

Source-backed tie map

This section follows the corrected sourcing rule: each tie is linked to a primary or near-primary source, and copied review articles do not count as independent corroboration.

- Semler / Brunell / Burnett: Semler DEF 14A names Brunell as a Bitcoin advocate/content producer and Burnett as a leading voice/influencer.

- Bailey / Nakamoto: KindlyMD/Nakamoto Exhibit 10.15 discloses consulting, bonus, option, and RSU economics.

- Pompliano / ProCap: SEC-filed Exhibit 99.1 discloses the $1 salary and performance-equity structure.

- Rochard / Strive: Strive Form 10-K lists Rochard as director and contains compensation disclosures to be table-extracted.

- Moss / Satsuma: Satsuma prospectus identifies the Chief Bitcoin Strategist role; exact economics need full parse.

- Ammous / Genius Group: SEC-filed Genius Group materials identify the board-advisor role; compensation not found yet.

- Pysh and Weiss / BitcoinTreasuries.net: official BitcoinTreasuries.net announcements identify the scoreboard-layer advisory roles; compensation is private/undisclosed.

- Livera / OranjeBTC: Bitcoin for Corporations lists the Investor/Advisor label; compensation or investment terms were not found in public filings.

Closing frame

Everybody has an angle.

This one brought a cap table, a podcast feed, a conference badge, a data dashboard, a board seat, and a familiar voice explaining why the wrapper is still Bitcoin-native.

Maybe it is.

Maybe it is not.

The ties are public now.

Read them again.

---

- Trent Jones